(Objective 4-4) What organization is responsible for developing ethics standards at the…

(Objective 4-4) What organization is responsible for developing ethics standards at the international level? What are the fundamental principles of the international ethics standards?

(Objective 4-4)

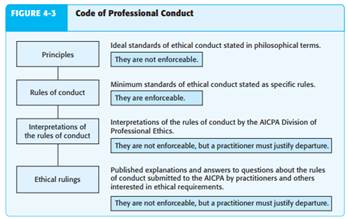

CODE OF PROFESSIONAL CONDUCT

The AICPA Code of Professional Conduct provides both general standards of ideal conduct and specific enforceable rules of conduct. There are four parts to the code: principles, rules of conduct, interpretations of the rules of conduct, and ethical rulings. The parts are listed in order of increasing specificity; the principles provide ideal standards of conduct, whereas ethical rulings are highly specific. The four parts are summarized in Figure 4-3 and discussed in the following sections. A few definitions, taken from the AICPA Code of Professional Conduct, must be understood to help interpret the rules.

• Client. Any person or entity, other than the member’s employer, that engages a member or a member’s firm to perform professional services.

• Firm. A form of organization permitted by law or regulation whose characteristics conform to resolutions of the Council of the American Institute of Certified Public Accountants that is engaged in the practice of public accounting. Except for the purposes of applying Rule 101, Independence, the firm includes the individual partners thereof.

• Institute. The American Institute of Certified Public Accountants.

• Member. A member, associate member, or international associate of the American Institute of Certified Public Accountants.

• Practice of public accounting. The practice of public accounting consists of the performance for a client, by a member or a member’s firm, while holding out as CPA(s), of the professional services of accounting, tax, personal financial plan – ning, litigation support services, and those professional services for which standards are promulgated by bodies designated by Council.

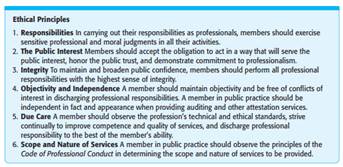

The section of the AICPA Code dealing with principles of professional conduct includes a general discussion of characteristics required of a CPA. The principles section consists of two main parts: six ethical principles and a discussion of those principles. The ethical principles are listed in the box above. Discussions throughout this chapter include ideas taken from the principles section. The first five of these principles are equally applicable to all members of the AICPA, regardless of whether they practice in a CPA firm, work as accountants in business or government, are involved in some other aspect of business, or are in education. One exception is the last sentence of objectivity and independence. It applies only to members in public practice, and then only when they are providing attestation services such as audits. The sixth principle, scope and nature of services, applies only to members in public practice. That principle addresses whether a practitioner should provide a certain service, such as providing personnel consulting when an audit client is hiring a chief information officer (CIO) for the client’s IT function. Providing such a service can create a loss of independence if the CPA firm recommends a CIO who is hired and performs incompetently.

Do you need a similar assignment done for you from scratch? We have qualified writers to help you. We assure you an A+ quality paper that is free from plagiarism. Order now for an Amazing Discount!

Use Discount Code "Newclient" for a 15% Discount!

NB: We do not resell papers. Upon ordering, we do an original paper exclusively for you.